From Critical Geopolitical Forces and Increasing Maturity, 2020 Has Been a Pivotal Year for the Drone Industry

In this post, I’ll illustrate some of the market trends over the past year using data from our fourth Drone Market Sector Report and describe forces that have shaped the drone industry.

While the report and market has seen significant changes across the board, if we were to distill the key forces impacting the market in 2020, they break down into these four:

- Business adoption matures

- Security concerns around Chinese-made products

- Hardware market becomes more interesting

- COVID-19’s unequal impact

Force 1 – Business Adoption Matures

As we’ve seen in our recent report on the FAA’s registration data, the larger drone market is shifting increasingly towards industrial applications, and this is reflected in our data with an increased proportion of business and agency users.

Among these users, we are seeing more of their drone operations being mature, both in terms of integration with regular operations and how long they have been deploying drones.

This maturity is reflected in their budgets, with spending on drones and drone-related services increasing significantly among those with a drone program for two years or longer.

Despite this growth and maturity, we aren’t necessarily seeing the explosion that many forecasts have predicted years before, with fleets remaining at moderate sizes.

There is money to be made here for vendors and service providers, but it’s through identifying the right market vertical and providing real value, not riding a massive drone wave.

Force 2 – Security Concerns Around Chinese-Made Products

Over the past several years, we have seen increased concern about the security of Chinese-made products. Some claims are made about specific brands, and others more generally about “data flows” to foreign nations, and China in particular.

Our 2020 Drone Market Sector Report breaks down the impact these claims are having across drone buyers and service providers.

Among drone buyers, we have seen widespread awareness of these claims, and that – while the majority were not impacted – over a quarter (27%) of all drone buyers were impacted by these security claims. Of those impacted, they were more likely to see these concerns slow or pause their purchases (58%) instead of driving them to alternative products (42%).

Just below one-fifth (19%) of all service providers were impacted. Of those impacted, they were slightly more likely to have moved to alternative products already (54%), but those who didn’t switch reported that these concerns lost them projects or clients (46%).

If the unspoken goal of these claims is to drive drone hardware market share to domestic players, there is some evidence that it is working, but our data suggests the negative side effects outweigh the “benefits”.

Force 3 – Hardware Market Becomes More Interesting

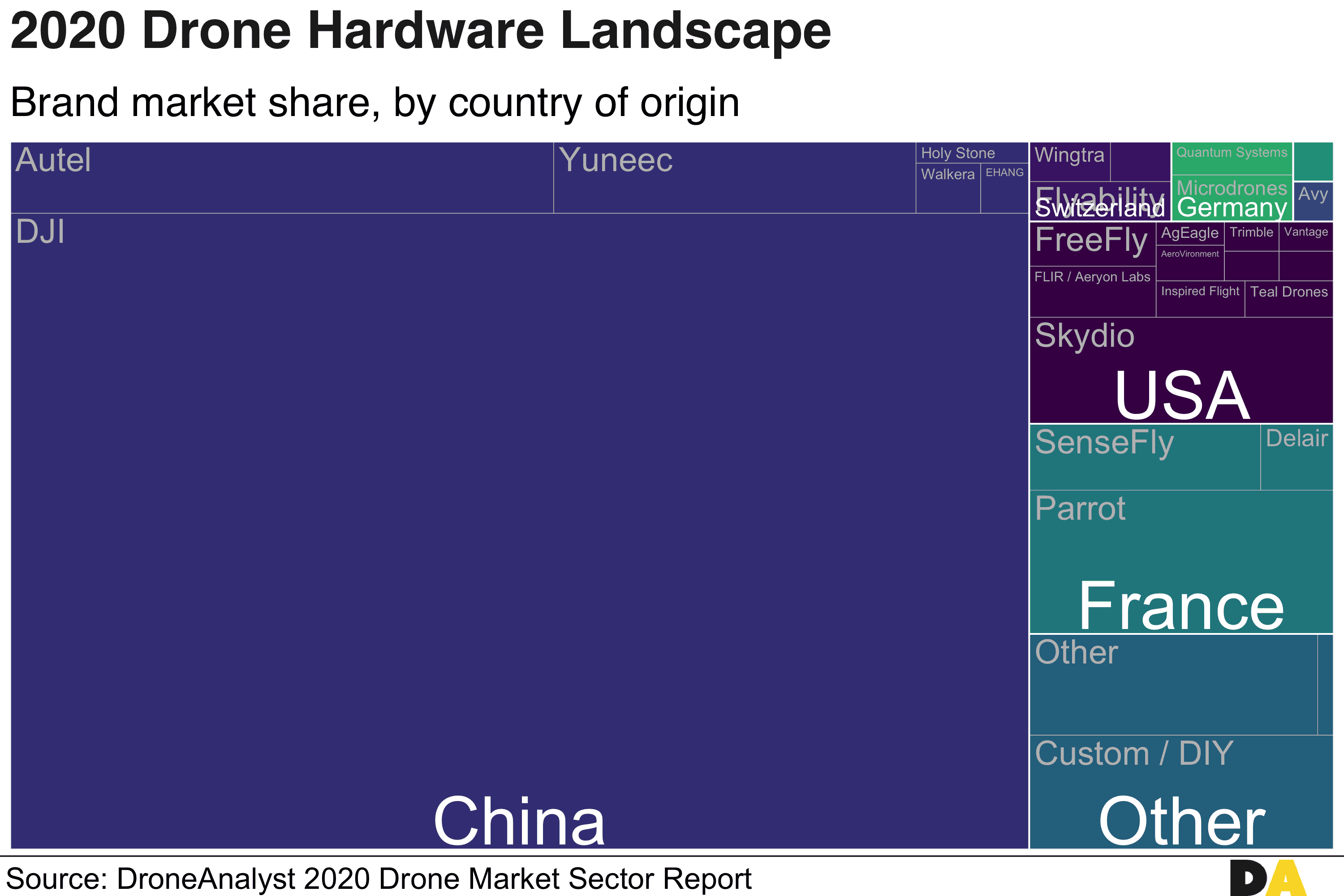

Ever since we started collecting drone market share data, DJI has remained at the top of the market, first at 50% in 2016 before climbing to 72% in 2017 and eventually 74% in 2018.

Today, we have found that DJI remains dominant, but new market players and security concerns have knocked them down a peg, dropping their market share to 69%.

This movement is driven by trends around hardware competition and geopolitical shifts raised in our earlier 2020 trends article, and it is telling that we are already starting to see these trends reflected in our market data.

With drone hardware playing a part in the larger US-China trade war, we have created a map showing hardware market share grouped by the manufacturer’s country of origin. Note that Country of Origin is based on the location of each firm’s headquarters, not where their drones or components are necessarily manufactured in.

This shows that China is by far and away the leader in sUAS manufacturing and development, with 77% of the market. France edges ever so slightly ahead of the US, with France’s drone ecosystem dominated by the Parrot Group.

Possibly the most interesting piece of this map is the makeup of America’s new drone ecosystem, now dominated by drone startups and led by autonomous drone maker Skydio. American manufacturers were previously led by 3D Robotics, who was 3rd globally in drone market share just two years ago and has since pivoted entirely towards software and partnering with China’s Yuneec on hardware.

Force 4 – COVID-19’s Unequal Impact

COVID-19 has had immense impacts across all sectors of the global economy. To begin to understand the impacts among the drone industry, we looked at the impact COVID-19 has had on service providers and business/agency users of drones or drone services.

Among these two groups, we saw one common thread, the overwhelming majority reported moderately negative impacts, with a small fraction of the market being positively impacted. Those most likely to report positive impacts were large service providers/networks and organizations that were most mature in their drone operations, with larger budgets and utilizing drones for several years.

Learn More with The Full Report

Our online survey garnered over 1,300 respondents, representing 39 industries across 110 countries. Our report uncovers insights from this dataset, with four sections that correspond to the four major segments of the drone industry:

- Drone aircraft and payloads purchased

- Service providers that offer drone-based imaging or sensing services for outside hire or sale

- Businesses and public agencies with drone programs

- Software apps or online services for drone operations and imaging

The report features 67 Figures and 10 Tables to uncover insights across these segments. We offer insights and analysis on:

- Who’s buying what types of drones from which makers at what prices and for what uses.

- How large the drone-based service providers are, and how they position themselves to their target industries.

- Who the business users of drone-based projects are, and which industries have traction.

- How much service providers, business users, and public agencies are using drone operations management and insights/analytics software, and the landscape of these software categories.

Exciting

Definitely, what a great blog and revealing posts, I definitely will bookmark your site. Best Regards!