Chinese drone players may celebrate the death of a federal procurement ban, but the US government will continue to support the birth of a new US Drone Hardware Ecosystem.

As the National Defense Authorization Act nears completion, the drone industry has watched closely as the Senate overrode a clause in the House of Representatives version of the bill that would ban the purchase of Chinese drones.

EDIT: Recently the US Commerce department has added China’s DJI, the industry’s leading drone manufacturer, to its blacklist, effectively banning them from procuring US-made tech to manufacture their drones. DroneDJ has more information on the specifics of this ban.

While this shift will cause dramatic shifts in the way businesses purchase drones and which vendors succeed in the market, it is just the last step in a number of geopolitical pressures and governmental action that. have had a widespread impact on the drone industry. We at DroneAnalyst have conducted research to understand the impact and how these changes are birthing a new US drone ecosystem.

New US Drone Ecosystem

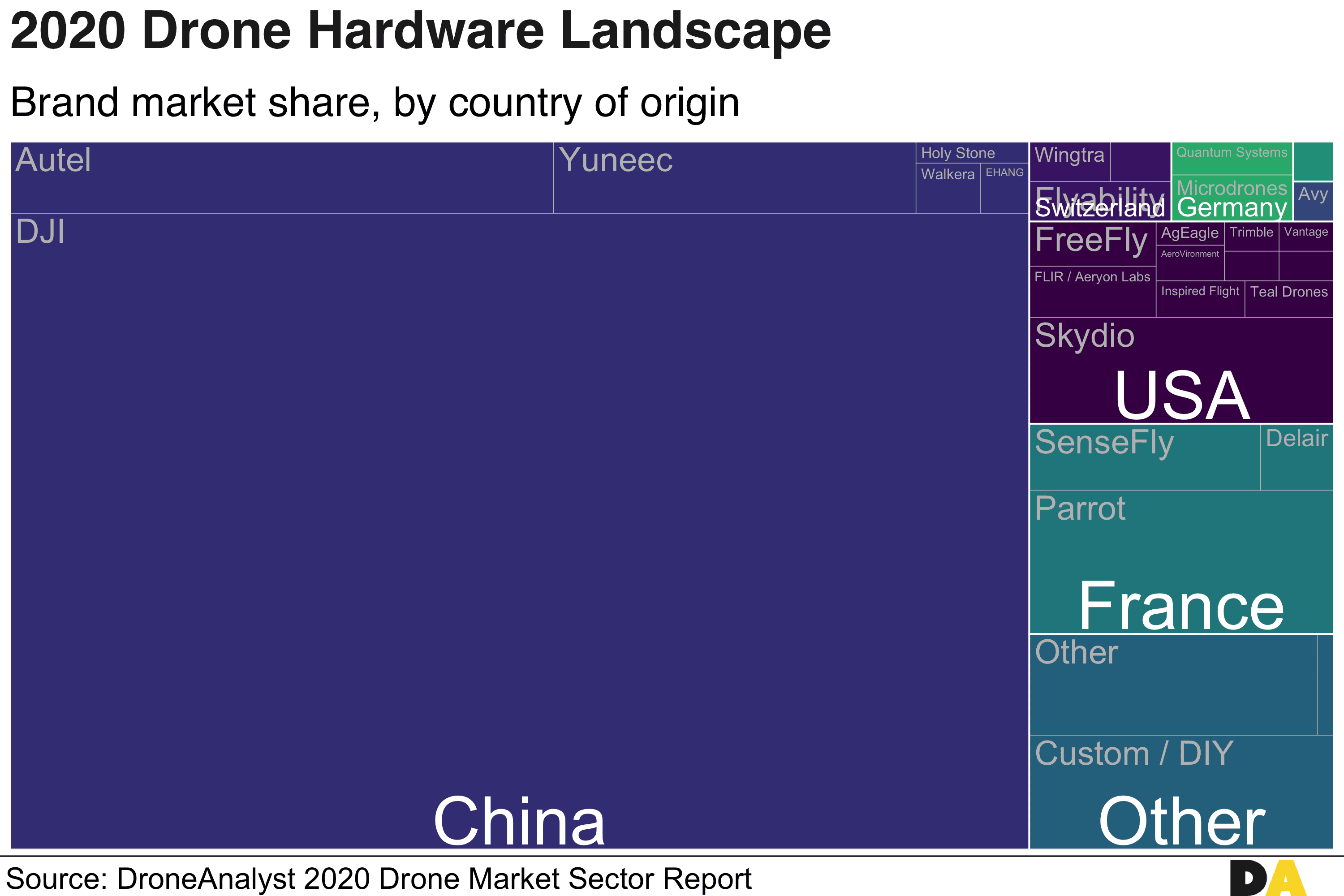

The story of the drone industry’s growth is also the story of Chinese DJI’s dominance. Rising from a 50% market share in 2016, to 74% in 2018, we have seen consumers, businesses and militaries alike choose DJI products due to their ease of use, reliability and low cost.

While DJI’s dominance remains the story in 2020, it is the first time we are seeing them weakened, with their market share dropping to 69%. A major cause of this drop is political pressures catching up with the company and the rise of a new US Drone Ecosystem.

While autonomous drone-maker Skydio is the only standout player among the young American upstarts, we are seeing a broader resurgence of US manufacturers after earlier drone hardware exits from 3D Robotics and GoPro. These new firms – such as FreeFly, FLIR (through Altavian and Aeryon Labs), Inspired Flight, Teal Drones and Vantage Robotics – are generally focused on the commercial and military market segments.

This rebirth is captured by a return to a 6.9% share of the global market, back to 2017 levels when 3D Robotics was the third most chosen brand globally and an uptick from 4% in 2018. We visualised just how much the US drone hardware ecosystem has changed in the animated map below.

But what is causing this resurgence, and is it here to stay?

Policies Supporting Domestic Growth

Although the US government has yet to take any legislative action that overly supports domestic manufactures, the Trump administration has seen several Federal agencies directly impact the market and cause secondary effects by raising broad security claims.

Security claims about the risks of Chinese drones have risen as early as 2017, from a leaked DHS memo. This has grounded Chinese-drone fleets at the DOI and has led to an informal ban on the use of Chinese drones over federal land.

Our recent research shows that these security claims – often that the drone data is being stored and shared with the Chinese government – are impacting the industry more broadly, influencing 27% of all drone purchases. While more than half (58%) paused or slowed their purchases, the remaining 42% found US-made alternatives. This signals that these claims have driven increased market share to domestic players but have had a net negative impact on the drone industry.

Alternatively, we have seen the DoD support domestic players directly, helping to secure funds for new players and creating a Blue sUAS group to ease federal procurement of US-made hardware.

These actions have had an impact and created an opportunity for domestic players, now it is up to these startups to capture market share through innovation. Security claims may have created short term benefits, but we hope to see the DHS and security experts better lay out steps that businesses can take to secure their operational data.

As the Biden administration comes into place at the start of next year, we suspect they will look favourably at continuing the prioritisation of domestic players through federal procurement and contracts. This is captured by Biden’s “Made in All of America” economic plan which calls for bringing back critical supply chains to the US through procurement strategies.

It begs to question if clauses banning Chinese-made drones may be wholly unnecessary, as other procurement guidelines may fundamentally make procuring US drones simpler and more effective for US agencies.

Our insights on the US hardware landscape are just a small sliver of insights gleaned from our 2020 Drone Market Sector Report. This report is designed for firms looking to learn more about which industry vendors are succeeding and where opportunities exist in the drone market. You can learn more or purchase a license to the report here.