The Start of 2021 Has Revealed Winners and Challenges Behind the Shift to a US Domestic Drone Industry

As we have revealed last year, 2020 saw a resurgence in US drone manufacturers, recouping lost market share by reaching similar levels as 2017. Despite this shift, the industry is still far away from both broad competition or a truly independent US supply chain.

The gap in the market development was made clear by the Office of the Secretary of Defense & Industrial Policy Office’s FY2020 Industrial Capabilities Report to Congress, which explores the relationship between private industry’ capabilities and America’s national security. In their section on Aircraft, the Industrial Capabilities report provides insight into the state of the market, which we cover a few highlights of below.

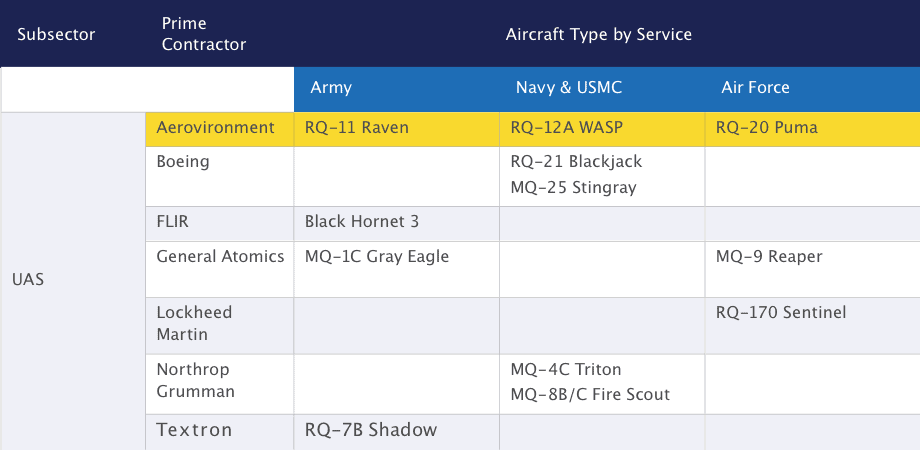

A Look at UAS Spending By the US Military

Military UAS have traditionally focused on fixed wing aircraft, spread across five groups with a large variation in weight and size. For reference, group 1 is classified as below 20 pounds and are similar in some aspects to what is deployed commercially for surveying applications. By comparison, group 5 is above 1,320 pounds and includes the much discussed Reaper that is used for tactical strikes. While much attention has been paid to the US-made micro-UAS quadcopter segment, the US military has primarily focused on more traditional fixed wing aircraft. Below is a chart of existing fleets by service. FLIR’s Black Hornet 3 (a heli design) is the only micro-UAS listed.

UAS and tactile missile system developer Aerovironment is notably the only player with an aircraft deployed by each service. This focus has been rewarded by a 23% increase in their UAS revenues from FY2019 to FY2020.

As is evidenced above, the US DoD has adequate industry capabilities when it comes to these more tried and tested form factors, but lacks broad availability of Small UAS. Therefore, the report spends much of its time discussing challenges among the Small UAS class.

Troubles Among Blue sUAS Offerings

As we’ve written about before, the establishment of the Blue sUAS group by the Defense Innovation Unit (DIU) has spurred competition among the thermal-enabled all-in-one quadcopter segment to provide alternatives to DJI’s Mavic 2 Enterprise Series. With the finalization of the five Blue sUAS drones – from Skydio, Vantage Robotics, Altavian, Teal Drones and Parrot – in August 2020, we have seen a few of these models hit the broader commercial market.

The original plan was for these drones to be inexpensive, US-made alternatives that can compete in the market. From our initial conversations with distributors and leading adopters in the US, Parrot, Teal and Skydio have reached the market, but all have encountered minor hiccups or limited availability along the way.

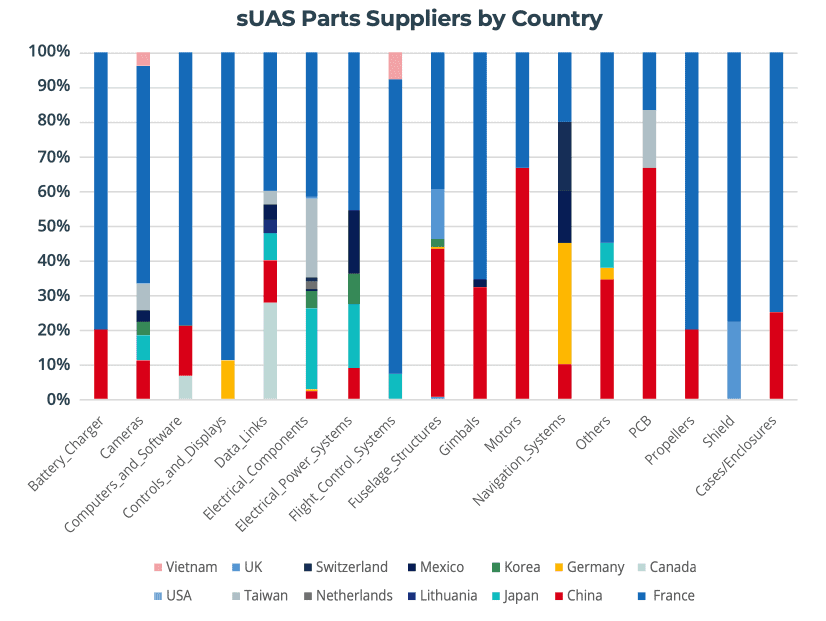

What is more surprising is that most of these drones may not fully be “Made in the USA”, at least according to the DoD’s report. They assessed the bill of materials of four unnamed US sUAS platforms – which we assume are part of the Blue sUAS Group – and found a significant amount of Chinese components in all of them. Some of these areas, like the fuselage structure, are of little importance but hint at the broader struggles to sourcing affordable, quality components in the United States. The report provided a graph of components of these four drones by country of origin, which we have included below.

This raises the broader question of whether or not most of these drones meet new federal rules on component sourcing, or if many of these drones need a waiver to be purchased. Recent rules include Trump’s Executive Order and Section 848 of the FY20 NDAA bill that have both put limits on federal agencies purchasing (or using) certain drones, mostly those with Chinese components. While the terminology across these two rules and the above chart are not entirely consistent, having gimbals, cameras or computers/software of Chinese origin would not be acceptable. It is more likely that agencies are currently getting around these limitations through waivers or, in the case of Trump’s EO, outlined steps to mitigate risks related to operating foreign made UAS.

While we won’t go on a wild goose hunt to guess which models are more or less “American”, potential buyers can likely guess based off of each firm’s marketing materials, as some are more specific around being “Section 848 compliant”.

These supply chain issues likely go deeper and we estimate that many of the selected manufacturers haven’t yet been able to steadily deliver units. This is speculation based on the DIU’s recently issued Blue sUAS 2.0 solicitation, which looks for more modular platforms, and specifies a manufacturer needs to be able to make more than 10 units per month.

All this goes to show that building up a domestic production capability that is commercially competitive is difficult, and is going to take time. As we can already see based on which parts are predominantly made in the US, there is intelligent prioritisation happening.

Importance of the US Military Market

If we turn the clock back just one or two years, many in the industry will find it unbelievable that these military-focused products may have broader commercial appeal. Today, the gap is closing on price and capability between what the military is using and what is available in the market, albeit only in a narrowly defined product segment. The market still has no real competition to DJI’s sub $900 consumer drones, all-in-one surveying drone (P4 RTK) or larger ruggedized platform (M300 RTK, although the Blue sUAS 2.0 and FreeFly Astro have this segment in their sights).

The DoD’s report calls into question the impact they have on the market, having allocated $153 million to its sUAS program in FY2020, out of its $3.2 billion UAS budget. Their assessment is based off of a bloated $4.2 billion market estimate of the U.S. small drone market. By our estimation that is severely off-base and overestimates the amount of drones sold into the market. We’ll be releasing an official market size later in April, but we estimate that the US military’s procurement budget as a portion of the U.S drone hardware market is 14%, not 4%. This better explains why many US hardware firms have flocked to the military sUAS segment, as it presents the largest opportunity in the market for them.

Where to Find More Insights

- Dive into the new US Drone hardware ecosystem

- Understand recent regulations from the FAA on Remote Identification.

- Learn how DJI’s drone dominance was born, the consumer market faltered and may rise again.

- See how COVID-19 has increased interest in consumer drones.

- Understand the four forces that shaped the drone industry in 2020.